Is KFC Going Out of Business?

Is KFC Going Out of Business as Kentucky Fried Chicken, is one of the most recognizable speedy-food manufacturers internationally. With ...

Read more

Do I Need a License to Start a Pressure Washing Business?

Do I Need a License to Start a Pressure Washing Business can be a profitable and flexible venture. With relatively ...

Read more

Is Tellurian Going Out of Business?

Is Tellurian Going Out of Business global nature of natural gasoline and strength, organizations like Tellurian Inc. play a critical ...

Read more

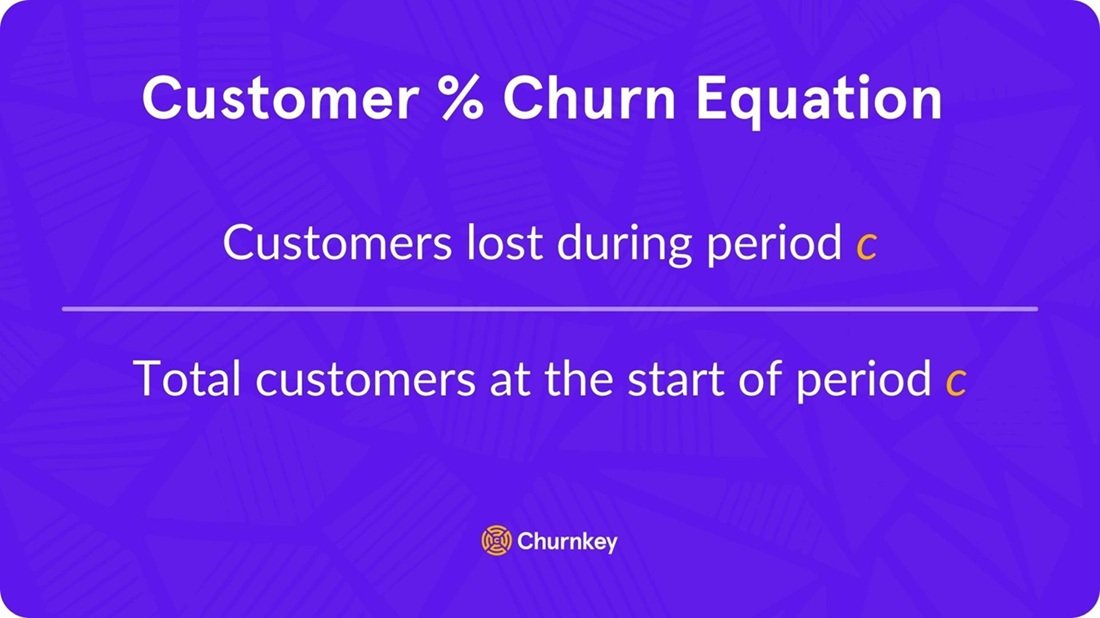

What Does Churn Mean in Business?

What Does Churn Mean in Business consumer retention is a vital metric that determines the lengthy-term health and profitability of ...

Read more

How to Start a Food Truck Business

How to Start a Food Truck Business is an exciting venture for culinary entrepreneurs who want to serve delicious food ...

Read more

Is Bath & Body Works Going Out of Business?

Is Bath & Body Works Going Out of Business is a well-known American retailer focusing on body care, home fragrances, ...

Read more

Is Minus Cal Still in Business?

Is Minus Cal Still in Business Cal gained interest within the well-being and nutrition area with its protein bars that ...

Read more

How to Start a Rental Business A Complete Step-by-Step Guide

How to Start a Rental Business is a smart way to generate passive income while meeting consumer needs without the ...

Read more

Is Redbox Out of Business?

Is Redbox Out of Business evolving digital enjoyment enterprise, businesses have to constantly adapt to live to tell the tale. ...

Read more

How to Start a Pest Control Business

How to Start a Pest Control Business can be a profitable and rewarding undertaking if approached with the proper understanding, ...

Read more